GST which is also known as VAT or the value added tax in many countries is a multi-stage consumption tax on goods and services.

GST is levied on the supply of goods and services at each stage of the supply chain from the supplier up to the retail stage of the distribution. Even though GST is imposed at each level of the supply chain, the tax element does not become part of the cost of the product because GST paid on the business inputs is claimable. Hence, it does not matter how many stages where a particular good and service goes through the supply chain because the input tax incurred at the previous stage is always deducted by the businesses at the next step in the supply chain.

GST is a broad based consumption tax covering all sectors of the economy i.e all goods and services made in Malaysia including imports except specific goods and services which are categorized under zero rated supply and exempt supply orders as determined by the Minister of Finance and published in the Gazette.

The basic fundamental of GST is its self-policing features which allow the businesses to claim their Input tax credit by way of automatic deduction in their accounting system. This eases the administrative procedures on the part of businesses and the Government. Thus, the Government’s delivery system will be further enhanced.

We need to pay taxes so that the government can finance socio-economic development; which includes providing infrastructure, education, welfare, healthcare, national security etc.

"Over the past few decades, the worldwide trend has been for the introduction of a multi-stage GST system. Today, almost 90% of the world's populations live in countries with GST, including China, Indonesia, Thailand, Singapore and India."

Understanding GST

GST shall be levied and charged on the taxable supply of goods and services made in the course or furtherance of business in Malaysia by a taxable person. GST is also charged on the importation of goods and services.

A taxable supply is a supply which is standard rated or zero rated. Exempt and out of scope supplies are not taxable supplies. GST is to be levied and charged on the value of the supply.

GST can only be levied and charged if the business is registered under GST. A business is not liable to be registered if its annual turnover of taxable supplies does not reach the prescribed threshold. Therefore, such businesses cannot charge and collect GST on the supply of goods and services made to their customers. Nevertheless, businesses can apply to be registered voluntarily.

Almost all countries collect income tax, which is a percentage of what you earn as an individual. Another way the government gets revenue is by collecting tax from business operations, like sales tax and duties on items that are bought or sold.

We need to pay tax so that the government can operate. GST is one method of collecting taxes which works better than others.

Background

GST is not new

The concept behind GST was invented by a French tax official in the 1950s. In some countries it is known as VAT, or Value-Added Tax. Today, more than 160 nations, including the European Union and Asian countries such as Sri Lanka, Singapore and China practice this form of taxation. Roughly 90 percent of the world's population live in countries with VAT or GST.

Here are some of the tax rates of countries around the world who have implemented GST or VAT.

Malaysian Tax History

In Malaysia, our tax system involves several different indirect taxes:

Import duty

On goods brought into the country

Export duty

On goods produced for sale outside the country

Government Sales Tax

On a wide range of goods at the point of import or at the manufacturer's level, with four tax rates at 5%, 10%, 20% and 25%

Service Tax

On services provided by restaurants, hotels, telecommunications services, professional services by architects, engineers, lawyers etc.

Excise Duty

On luxury and 'sin' products such as automobiles, liquor, beer and tobacco products

The proposed GST will replace the Government Sales Tax and the Service Tax.

Current Consumption Tax

a) SALES TAX

Sales Tax was introduced on the 29th February 1972 as a single stage consumption tax, levied, charged and paid on goods manufactured in Malaysia and imported.

Currently, the rates of sales tax are as follows:-

Reduced rate of 5% for non-essential foodstuff and building materials

A general rate of 10%

Specific rates for petroleum products

Licensing

Manufacturers of taxable goods whose annual sales turnover exceed RM100,000 is required to be licensed under sales tax act. Those with annual sales turnover does not exceed RM100,000 are required to apply for a certificate of exemption from licensing.

Scope of Tax

Sales tax is levied on locally manufactured goods at the time the goods are sold or otherwise disposed of by the manufacturer. It is called a single stage tax because sales tax is to be charged once only, either at the input or at the output stage.

List of goods subject to sales tax at 10%

List of goods subject to sales tax at 5%

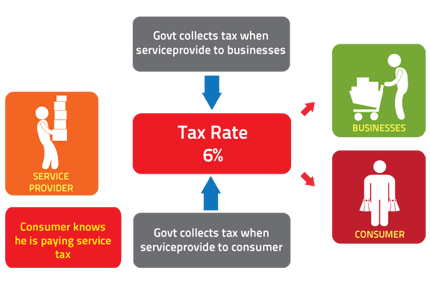

b) SERVICE TAX

Service tax was introduced on the 1st March 1975 as a single stage consumption tax, levied, charged and paid on specific services provided by a taxable person in Malaysia.

Currently, the rates of service tax are as follows:-

Flat rate of 5%;

Specific rates for credit card - RM50.00 (effective from 1st January 2010)